VA loan vs conventional loan in Texas: which is better for veterans?

A lot of Texas veterans walk into this decision with confident opinions already baked in, usually borrowed from a friend, a fellow service member, or a quick internet search. Some hear that a VA loan is always the right call because they earned the benefit. Others hear that a veteran with solid credit is leaving money on the table by not going conventional. I've seen both camps, and here's the honest answer: VA loans offer real advantages for most Texas veterans, but the better loan depends on your credit profile, how much cash you have available, the Texas market you're buying in, and how long you plan to stay. This article won't crown a winner. It will walk you through both options so you can figure out which one actually fits your situation.

Quick answer

For most Texas veterans, VA financing makes sense. Zero down payment potential, no monthly mortgage insurance, and flexible qualification standards are hard to beat, especially in high cost markets like Austin and Dallas-Fort Worth where a conventional down payment can take years to accumulate.

That said, conventional financing deserves a serious look if you have 20% or more saved, your credit score is in the 760+ range, you're dealing with a property type that creates VA eligibility complications, or you have strategic reasons to preserve your full VA entitlement for a later, higher value purchase.

Think of this as a decision matrix, not a verdict. The same veteran buying a $350,000 home in San Antonio on PCS orders from Joint Base San Antonio might reach a different conclusion than a veteran buying a $650,000 home in Austin after 20 years of disciplined saving. Both are valid scenarios. The math just looks different.

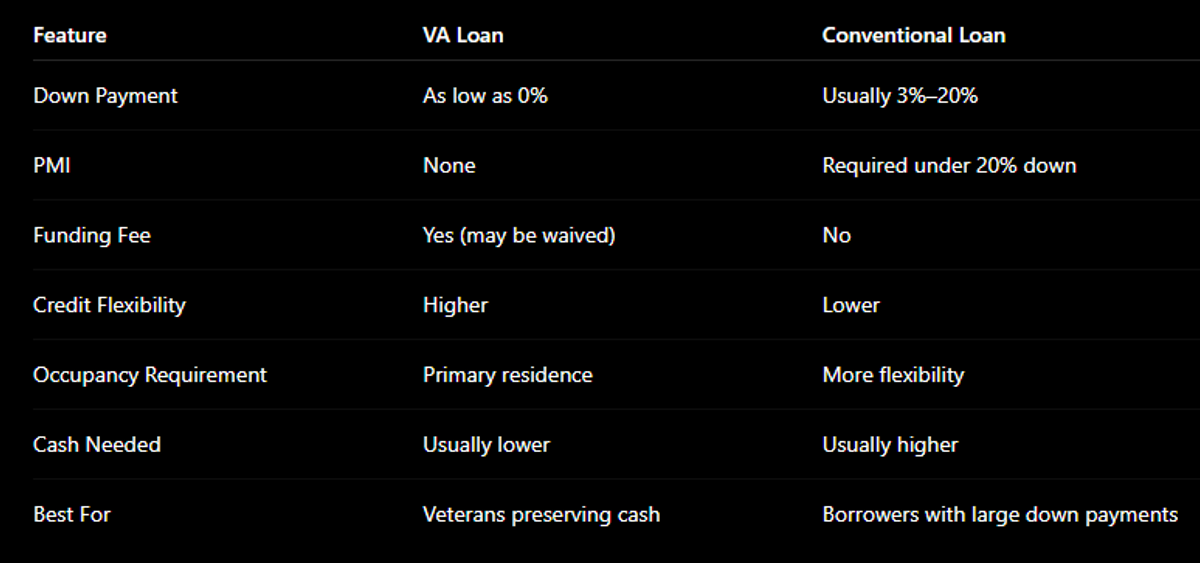

What is a VA loan?

The VA loan program exists because the federal government guarantees a portion of the loan on behalf of eligible veterans and service members. That guarantee reduces the lender's risk, which is what allows lenders to offer zero down payment and skip the monthly mortgage insurance requirement that comes with other low down payment options.

In practical terms: you can buy a Texas home with nothing out of pocket for the down payment, no monthly PMI added to your payment, and qualification standards that are generally more forgiving than conventional guidelines. The trade off is a one time VA funding fee (more on that shortly) and an occupancy requirement, meaning you need to intend to live in the home as your primary residence. If you're still learning how VA financing works overall, our Complete VA Loan Guide covers eligibility, entitlement, occupancy requirements, funding fees, closing costs, and the full Texas VA homebuying process.

Eligibility is based on your service history, discharge status, and in some cases your surviving spouse status. If you've used a VA loan before, the benefit can often be restored or used again. For a full breakdown of how eligibility works in Texas, see VA Loan Eligibility in Texas: What Veterans Need to Know. And if you're not sure whether you have a Certificate of Eligibility in place yet, How to Get a Certificate of Eligibility (COE) for a VA Loan walks through that process.

What is a conventional loan?

A conventional loan is private financing with no government guarantee behind it. Because the lender carries more of the risk, qualification standards are generally tighter, and borrowers who put down less than 20% are required to pay PMI.

PMI, or private mortgage insurance, is simply an extra monthly cost added to your payment to protect the lender in case you default. It's not insurance that benefits you. It typically runs somewhere between 0.5% and 1.5% of the loan amount per year, and it cancels once your loan balance drops to 80% of the home's value. On a $400,000 Texas home, that's roughly $167 to $500 per month added to your payment until you build enough equity to eliminate it.

Conventional loans follow conforming loan guidelines set by Fannie Mae and Freddie Mac. The conforming limit for most Texas counties in 2026 is $832,750. You can put as little as 3% down with certain conventional programs, though the lower your down payment, the higher your PMI cost and the more your monthly payment climbs. Strong borrowers, think 740+ credit, 20% down, can find competitive conventional terms. But the lower your score or down payment, the more the VA loan's structure tends to pull ahead.

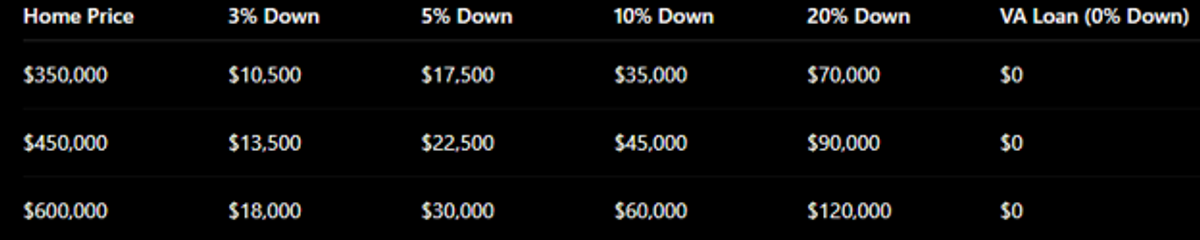

Down payment comparison: real Texas numbers

Here's what the cash requirement looks like for a conventional loan at different down payment levels, compared to the VA option, on three common Texas price points:

Keep in mind these are down payment figures only. Closing costs apply to both loan types.

For a veteran receiving PCS orders to Fort Cavazos, Joint Base San Antonio, or Fort Bliss, the timeline between receiving orders and needing to close is often tight. Building a conventional down payment isn't always realistic on that schedule. The ability to walk in with zero down, close within a reasonable timeframe, and keep cash in the bank has real practical value for relocating military families.

The cash you don't spend on a down payment also doesn't disappear into thin air. It stays liquid, available for an emergency fund, home repairs, or other financial goals. That's worth something, and I'll come back to it in the five year analysis below.

Monthly payment comparison: where VA often wins

The monthly payment advantage with VA usually comes down to one thing: no PMI.

On a $400,000 Texas home with 5% down on a conventional loan, you're adding PMI to your payment every single month until your balance drops to $320,000. Depending on your credit score and the lender's pricing, that PMI might run $150 to $350 per month on a loan that size. That's a line item that just sits there for potentially eight to ten years before it cancels.

With a VA loan, there's no PMI. Ever. The VA funding fee is a one time cost that most veterans finance into the loan balance rather than paying out of pocket. That adds a modest amount to the principal, but it eliminates the monthly drag of PMI entirely.

Here's a simplified comparison. Same $400,000 Texas home. Assume similar interest rates for both loans. Conventional with 5% down includes PMI; VA has no PMI but the funding fee is financed in.

- Conventional principal and interest + PMI: roughly $200 to $350/month higher than VA, depending on PMI rate and credit score

- VA principal and interest, no PMI: lower monthly cost, slightly higher starting balance due to financed funding fee

The gap closes if the conventional borrower puts down 20%, because PMI goes away. But for veterans using less than 20% down, VA almost always produces a lower monthly payment on the principal, interest, and MI portion.

One thing I want Texas veterans to understand: property taxes in this state can dwarf the difference between loan types. A $450,000 home in Travis County (Austin) carries an effective property tax rate around 2.1%, which adds roughly $787 per month to your payment before a single dollar of principal, interest, or insurance is counted. In Harris County (Houston), the effective rate sits in a similar range. Tarrant and Dallas counties aren't far behind. Bexar County (San Antonio) tends to run slightly lower, but still well above national averages.

The choice between VA and conventional might affect your payment by $100 to $300 per month. Texas property taxes often affect your payment by $600 to $900 per month or more. Make sure your affordability math accounts for both. The monthly payment calculator can help you model the full PITI picture before you commit to a price range.

I had a client come to me relocating to the DFW area who had done most of his homework online. He was comparing rates between VA and conventional and trying to decide which was the better deal. What he hadn't accounted for was the property tax difference between the two neighborhoods he was considering. One was in a lower tax suburban county; the other was inside a city with a higher combined rate. That tax difference alone was $280 per month, which mattered far more to his decision than the loan type itself. He ended up with a VA loan, but the more important lesson was understanding the full payment before falling in love with a list price.

For more on how buying power works with a VA loan specifically, How Much House Can I Afford With a VA Loan in Texas? goes deep on that math.

Credit score requirements: what Texas lenders actually expect

The VA itself sets no minimum credit score. That's true. But individual lenders add their own overlays, meaning their own internal minimums. Most Texas lenders require a 580 to 620 minimum to approve a VA loan, and some set it higher. The overlay exists because the lender still carries risk even with the VA guarantee behind the loan.

Conventional conforming loans generally require a 620 minimum, with the best pricing kicking in around 740. If your score is 680, you'll qualify for conventional, but you'll pay more for it than a borrower at 760.

Here's how that plays out practically:

- 580 to 619: VA is likely your only conforming option; conventional approval at this range is difficult

- 620 to 680: Both loan types may be available, but VA's more flexible underwriting often produces better terms

- 680 to 740: Conventional becomes more competitive, but VA still typically wins on monthly payment if you're putting down less than 20%

- 740+: This is where conventional pricing gets genuinely competitive; veterans in this range should run both scenarios

Credit score affects your interest rate on both loan types. A borrower at 680 and a borrower at 760 are not paying the same rate on either product. For a Texas-specific breakdown of how your score shapes your options, What Credit Score Is Needed for a VA Loan in Texas? covers the full picture.

The VA funding fee vs PMI: understanding the real tradeoff

The VA funding fee is a one time cost paid to the federal government, not to the lender, that helps keep the VA loan program funded without taxpayer money. The amount varies based on your service history, whether it's your first or subsequent use of the VA benefit, and how much you put down.

For most first-time VA users putting nothing down, the fee is 2.15% of the loan amount. Subsequent use bumps it to 3.3%. Put 5% or more down, and the fee drops. Veterans with a service connected disability rating may qualify for a full waiver. See VA Funding Fee Explained for the complete rate table and waiver details.

PMI works differently. It's not one time; it's a monthly cost that continues for years. On a $400,000 loan with 5% down and a mid range PMI rate of roughly 0.8% annually, that's about $267 per month. Over five years before PMI might cancel, that's roughly $16,000 paid into PMI alone.

The VA funding fee on a $400,000 loan at 2.15% is $8,600, financed into the balance. You're paying interest on that $8,600 over the life of the loan, but you're not writing a check for it monthly. In most Texas scenarios with less than 20% down, the VA funding fee becomes a better deal than years of PMI by year two or three.

Where this calculation flips: if you're putting 20% down on a conventional loan, PMI never appears. You're comparing the VA funding fee against nothing. In that specific scenario, the conventional loan structure has a real cost advantage.

When a VA loan usually makes more sense

- You're relocating on PCS orders from Fort Cavazos, JBSA, or Fort Bliss and don't have years to accumulate a conventional down payment

- You're buying in Austin or DFW where $450,000 to $600,000+ is a realistic price range and a 10% to 20% down payment represents $45,000 to $120,000 in cash

- Your credit score is solid but not exceptional, somewhere in the 620 to 700 range, and VA's more flexible underwriting produces better terms

- Preserving liquidity is a priority: keeping $40,000 to $80,000 in the bank rather than deploying it as a down payment has real financial flexibility value

- You want the lowest possible monthly payment without PMI dragging on it for years

A practical example: a veteran buying a $475,000 home in DFW with a VA loan needs $0 for the down payment. The same veteran going conventional at 10% down needs $47,500 before closing costs. That's a real number, and for many families it's the difference between buying this year and buying in three years.

When a conventional loan may make more sense

This section exists because I'd rather give you the full picture than steer you toward one product regardless of your situation.

Conventional financing deserves a serious look when:

- You have 20% or more saved and can eliminate PMI entirely. In that case you're comparing the VA funding fee against zero PMI. Conventional wins that specific math.

- Your credit score is 760 or above and you qualify for the most competitive conventional pricing. Run both scenarios; the gap may be smaller than you expect.

- The property type creates VA complications. Certain condo projects that aren't VA approved, mixed use properties, or situations involving investment considerations can make conventional the cleaner path.

- You want to preserve full VA entitlement for a future, higher value purchase. Veterans who expect to buy a more expensive Texas home in three to five years sometimes choose conventional now to keep their full VA benefit available later.

This is not an argument against VA loans. It's an acknowledgment that the math occasionally favors conventional for specific borrower profiles, and a good broker's job is to show you both sets of numbers before you decide.

Before you settle on either path, Texas VA Preapproval: What Veterans Should Know Before House Hunting is worth reading regardless of which direction you lean.

Common myths about VA loans Texas veterans still hear

Myth: VA loans are only for first-time buyers. The benefit has no first-time buyer restriction. Veterans can use it multiple times under the right conditions, and many do.

Myth: VA loans take longer to close and sellers won't accept them. Timelines vary by lender and market, not by loan type. An experienced buyer's agent and a solid preapproval letter remove most of the seller resistance I've seen in competitive Texas markets. The perception exists, but it's manageable.

Myth: Using your VA benefit once means it's gone. Entitlement can be restored after payoff, and bonus entitlement allows some veterans to carry two VA loans simultaneously. The rules are specific, but the benefit is far more flexible than most veterans realize.

Myth: Veterans with great credit should always choose conventional. Credit score is one variable. Down payment, PMI, and monthly payment goals matter just as much. A 760 credit veteran putting 5% down may still see a better total payment with VA than conventional.

Myth: Conventional offers are always stronger for sellers. In most Texas transactions, purchase price, earnest money, and a clean preapproval matter more to sellers than loan type. A well-prepared VA offer is competitive.

Which loan leaves you in a stronger position five years from now?

I think this is the question veterans should be asking, and most aren't.

Consider two veterans buying the same $450,000 Texas home. One uses a VA loan with zero down and keeps $50,000 in savings. The other uses conventional with 20% down ($90,000) and eliminates PMI. Five years in, assuming modest Texas appreciation of around 3% annually, both veterans have similar equity positions from price appreciation. The conventional borrower has paid down slightly more principal, but the VA borrower kept $50,000 to $90,000 liquid for those five years. That cash funded an emergency fund, covered a roof repair, or sat in an account generating returns.

The monthly payment difference also compounds over time. PMI savings with conventional (versus VA zero-down) only exist if you avoid PMI by putting 20% down. And deploying $90,000 as a down payment has an opportunity cost that rarely gets discussed.

There's no universally correct answer here. A veteran who depletes their savings on a down payment and then faces a $15,000 AC replacement or a job change in year two is in a tighter position than one who kept that cash available. The best loan is the one that supports your financial strategy over five years, not just the one with the lowest quoted rate on day one.

How to decide which loan is right for you

Run through this decision framework honestly:

- How much cash do you have available? If you're under 20% down, VA typically wins on monthly payment.

- What is your credit score? Below 700, VA's flexible underwriting is usually the better fit. Above 740, run both scenarios before deciding.

- How long do you plan to stay? A longer hold period increases the value of no PMI. A short hold might favor a different calculation.

- Do you have future VA loan plans? If you expect to buy a significantly higher value Texas home in the next few years, entitlement strategy matters.

- What does the full payment look like? Include principal, interest, PMI or no PMI, funding fee if financed, Texas property taxes for the specific county, and insurance. The mortgage payment calculator can help you model the full picture.

The right answer in Austin with a $550,000 home price and Travis County tax rates may look different from the right answer in El Paso with a $300,000 home price and lower effective tax rates. Texas is not one market; it's several.

Texas is not one market. Property taxes, home prices, insurance costs, and local conditions can change your buying power dramatically from one city to the next. Find Out How Much Texas Home You May Be Able To Afford

Complete our Get My Texas VA Buying Power questionnaire and we'll help you understand your financing options before you start shopping.

Frequently asked questions

Is a VA loan better than a conventional loan in Texas?

For most Texas veterans, VA financing offers meaningful advantages: no down payment requirement, no monthly PMI, and generally more flexible qualification standards. In high cost Texas markets like Austin and Dallas-Fort Worth, where a 10% to 20% conventional down payment represents $45,000 to $120,000 or more, the VA option lets veterans buy sooner and keep more cash in reserve. That said, "better" depends on the individual. Veterans with 20% or more saved, 760+ credit, or specific property or entitlement considerations may find that conventional financing makes more sense for their situation. The honest answer is that both options deserve a side by side look before you decide.

Why do some veterans with strong credit still choose conventional financing?

The main reason is the 20% down payment calculation. If a veteran can put 20% down on a conventional loan, PMI never enters the picture. At that point, the comparison becomes the VA funding fee versus zero PMI, and conventional can win that math. Some veterans also choose conventional to preserve full VA entitlement for a future, higher-value purchase. A veteran buying a smaller starter home today with conventional financing keeps their full VA benefit available when they're ready to move up to a more expensive property in Austin or DFW.

Does a VA loan always result in a lower monthly payment than conventional?

Not always, but often. The no PMI advantage is the primary driver. For veterans putting less than 20% down, VA almost always produces a lower principal, interest, and MI payment because PMI never appears on the statement. For veterans putting exactly 20% down on a conventional loan, PMI is gone and the comparison shifts. In that case the monthly payment gap between loan types typically narrows or disappears. Texas property taxes, which can run $600 to $900 or more per month on a mid range home, affect the total payment equally regardless of loan type and often matter more to affordability than the financing choice itself.

Can I avoid PMI on a conventional loan, and how does that compare to the VA funding fee?

Yes. Put 20% or more down on a conventional loan and PMI doesn't apply. That changes the comparison significantly. Instead of paying years of PMI versus a financed VA funding fee, you're comparing the funding fee against zero additional insurance cost. On a $450,000 purchase, the first-use VA funding fee at zero down is roughly $9,675 financed into the loan. If you could have put 20% down conventionally and avoided PMI entirely, the conventional structure may cost less over the life of the loan. For veterans with less than 20% down, though, the funded VA fee is almost always cheaper than several years of monthly PMI payments.

Which loan requires less cash at closing for a Texas home purchase?

VA, in most cases, by a significant margin. The VA loan requires no down payment from eligible veterans. Closing costs still apply, and those can sometimes be covered through seller concessions or lender credits. Conventional loans require a minimum 3% down for some programs, though 5% to 10% is more common, and down payments up to 20% eliminate PMI. On a $450,000 Texas home, the difference between VA and a 10%-down conventional loan is $45,000 in out of pocket cash before closing costs are even factored in. For veterans on PCS timelines or those who haven't had years to accumulate savings, that gap is often the deciding factor.

Can I switch from a conventional loan to a VA loan after closing?

Not a straight switch. Once a loan is closed, that's the structure you have. However, if you currently have a conventional loan and you're VA eligible, you can refinance into a VA loan. This would be a VA cash out refinance, which allows eligible veterans to refinance a non VA loan into a VA loan and potentially access equity at the same time. It's not the same as simply converting the loan, but it is a path available to veterans who closed conventionally and later want to take advantage of their VA benefit.

Does the VA funding fee make conventional loans cheaper overall?

In some scenarios, yes. The funding fee is a real cost, typically 2.15% of the loan amount for first-time VA users with no down payment. On a $400,000 loan, that's $8,600 added to the balance. If you're comparing that to a conventional loan with 20% down and no PMI, conventional can be the cheaper structure over the full loan term. But if you're comparing the funding fee against years of monthly PMI payments on a conventional loan with less than 20% down, the math usually favors VA by year two or three. The funding fee is a one time cost. PMI is a monthly cost that continues until your loan to value drops to 80%, which can take many years depending on your down payment and the pace of Texas home price appreciation.