VA funding fee explained: what veterans pay and when it's waived

A veteran I worked with was reviewing his Loan Estimate when he spotted a line item he didn't recognize: "VA funding fee." His first reaction was that his lender had tacked on a junk fee and he wanted it removed. That reaction is completely understandable, and it's one of the most common misconceptions I see veterans run into during the loan process. Here's the short answer: the VA funding fee is not a lender fee. It goes directly to the Department of Veterans Affairs, not to your broker or your lender. Your lender cannot pocket it, negotiate it away, or waive it at the closing table. And some veterans owe nothing at all.

In this post I'll answer the four questions veterans ask me most often about this fee: what it is, how much it is, whether it can be rolled into the loan, and how to know if you're exempt. If you're still learning how VA financing works overall, our Complete VA Loan Guide covers eligibility, entitlement, occupancy requirements, funding fees, closing costs, and the full homebuying process.

What is the VA funding fee?

The VA funding fee is a one time charge paid to the Department of Veterans Affairs when you use a VA backed loan. It appears on your Loan Estimate as a government charge, which is why it sits separately from lender fees and origination charges. That placement is intentional and accurate. The lender collects it at closing and forwards it to the VA. They have no authority to reduce it, waive it, or keep any portion of it. Because the funding fee appears alongside other settlement charges, many veterans confuse it with closing costs. Our VA Loan Closing Costs Explained guide breaks down the difference.

The fee applies to VA purchase loans, VA cash out refinances, and VA IRRRLs (streamline refinances). Each of those loan types carries its own rate structure, so the percentage you owe depends on what kind of transaction you're doing, how much you're putting down, and whether this is your first time using a VA loan benefit.

Because it's a government charge set by federal statute, shopping around to different lenders will not change the fee. What changes it is your eligibility status, your down payment amount, and your prior use of VA loan benefits.

Why does the VA charge a funding fee?

The VA loan guaranty program is self funded. The funding fee is what keeps it operating without requiring annual taxpayer appropriations from Congress. That distinction matters because it means the program isn't dependent on the federal budget process to stay alive.

Think about what the VA loan program offers: no down payment required, no monthly private mortgage insurance, competitive rates, and no prepayment penalty. Those benefits exist because the VA guarantees a portion of every loan to the lender, reducing their risk. The funding fee is what finances that guaranty. Without it, either those benefits would shrink or the program would need direct taxpayer funding.

The fee has been part of the program since its post World War II origins and has been adjusted by Congress multiple times over the decades. The honest tradeoff is this: you pay a one time fee upfront, or finance it into the loan, in exchange for long term savings that most conventional loan options cannot match. For most veterans I've worked with, that math works strongly in their favor.

Who has to pay the VA funding fee?

Most veterans, active duty service members, and eligible surviving spouses who use a VA loan are required to pay the funding fee. That includes first time users and borrowers using their VA benefit again after a previous VA loan. Those borrowers must also satisfy the VA's owner occupancy requirements when purchasing a home with VA financing. Our VA Loan Occupancy Requirements Explained guide covers those rules in detail.

Reservists and National Guard members are also subject to the fee, though their rates have historically differed slightly from regular military. As of the most recent Congressional adjustments, those rates have been aligned more closely with regular military rates, but it's worth confirming your specific category when you apply.

Borrowers using a VA IRRRL or a VA cash out refinance also owe a funding fee, though the rates are structured differently from purchase loans. The rate for a cash out refinance is higher than a purchase loan rate, which surprises some veterans who assume the fee only applies when buying a home.

Whether you actually owe the fee depends on your disability status and military category. That question leads directly to the most important section below.

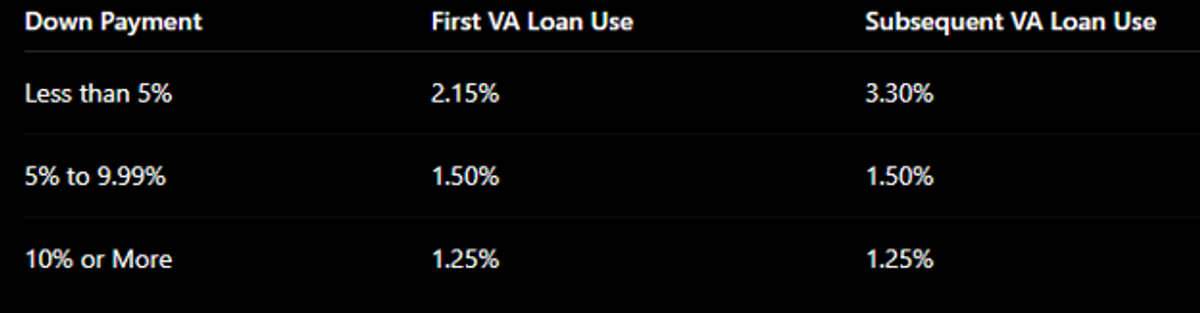

Current VA funding fee rates

For VA purchase loans, the fee is calculated as a percentage of the loan amount. The rate depends on two variables: whether this is your first use of a VA loan benefit or a subsequent use, and how much you're putting down.

The funding fee percentages below reflect current rates at the time this article was published. Because Congress can change these rates, it's always worth confirming current funding fee percentages before making a final financing decision.

Purchase loan rate structure:

To put real numbers on that: if you're buying a $350,000 home with no down payment on your first VA loan, the funding fee is 2.15% of $350,000, which comes to $7,525. If this is your second time using a VA loan with no down payment, the rate jumps to 3.30%, putting the fee at $11,550. That's a meaningful difference, and it's one reason some veterans choose to put at least 5% down on a subsequent-use loan.

VA IRRRLs carry a flat funding fee of 0.50% of the loan amount, which is significantly lower than purchase and cash out rates. VA cash out refinances are subject to the same first use and subsequent use rates as purchase loans.

These rates are set by federal law and are subject to change by Congress. I'd encourage you to use the VA Loan Calculator on this site to run current numbers for your specific scenario.

Who qualifies for a VA funding fee waiver?

This is the section that matters most if you're not sure whether you owe the fee at all.

Veterans receiving VA compensation for a service connected disability are exempt from the funding fee, regardless of their disability rating percentage. A 10% rating qualifies just as much as a 100% rating. This is one of the most widely misunderstood points in the entire VA loan process.

Veterans who have a proposed or memorandum disability rating at the time of closing are also exempt, even if they are not yet receiving compensation. If your claim is pending and a rating decision has been issued but not finalized, that can still qualify you for the waiver. I've seen veterans pay this fee unnecessarily because they didn't know about the pending rating exemption. Make sure your lender knows the status of your claim before closing.

Active duty service members who have been awarded the Purple Heart before or on the closing date are exempt. The award date matters; if it's awarded after closing, the exemption doesn't apply retroactively unless you file for a refund (more on that in the FAQ section).

Surviving spouses of veterans who died in service or from a service-connected disability, and who are using VA loan benefits as an eligible surviving spouse, are also exempt from the funding fee.

Practically speaking, the lender pulls your funding fee exemption status directly from your Certificate of Eligibility. If your COE doesn't reflect your current disability status because your claim was recently approved or your rating changed, contact the VA before closing to get that updated. Paying a fee you legally don't owe is avoidable, but only if you catch it before the loan closes.

Can the funding fee be financed into the loan?

Yes. VA rules allow you to roll the entire funding fee into the loan balance rather than paying it out of pocket at closing. For many veterans, especially those using the no down payment option, this is the most practical choice.

Here's what that looks like in dollar terms. On a $350,000 purchase with a first-use, no down payment funding fee of 2.15%, the fee is $7,525. Financed into the loan, your actual loan balance becomes $357,525 rather than $350,000. That higher balance is what you're paying interest on for the life of the loan.

Financing the fee is permitted under VA rules even though the loan amount will exceed the purchase price. That surprises some borrowers, but it's a standard feature of the VA program, not a workaround.

The honest tradeoff: if you can pay the fee at closing, you eliminate that additional interest cost over time. If cash conservation at closing is the priority, financing the fee is a reasonable and widely used option. Neither choice is automatically right; it depends on how long you plan to hold the loan and what your cash position looks like at closing.

How the funding fee affects monthly payments

Let me walk through a concrete example so you can see the actual payment difference.

A veteran buys a $350,000 home with no down payment on a first VA loan. The funding fee is 2.15%, or $7,525. If he finances that fee, his loan balance is $357,525. At a 30-year fixed term, that additional $7,525 in loan balance adds roughly $40 to $45 per month to his payment compared to a loan balance of $350,000, depending on the rate.

Now take a veteran in the same scenario who qualifies for a funding fee waiver due to a service connected disability. Her loan balance stays at $350,000. Same purchase price, same interest rate, meaningfully lower payment over the full loan term.

Over 30 years, the difference compounds. That's why confirming your waiver status before closing is worth the effort. Run your own numbers using the VA Loan Calculator to see what the impact looks like for your specific loan amount.

VA funding fee vs. PMI: which costs more?

This comparison comes up constantly when veterans are deciding between a VA loan and a conventional loan with a low down payment.

On a conventional loan with less than 20% down, the lender requires private mortgage insurance. PMI typically runs between 0.5% and 1.5% of the loan amount annually. On a $350,000 conventional loan, that translates to roughly $145 to $437 per month, every month, until you reach 20% equity.

The VA funding fee is a one time cost. PMI is a recurring monthly expense that accumulates. On a $350,000 loan with a 1% PMI rate, you'd be paying around $292 per month. Within about two years, the cumulative PMI cost surpasses a first use VA funding fee of $7,525. After five years, the PMI total would be approaching $17,500.

The honest exception: a veteran putting 10% or more down on a conventional loan may avoid PMI entirely and would also face a lower VA funding fee if using VA financing. In that scenario, the conventional loan might be competitive. The comparison isn't always automatic, and it's worth running both scenarios before you decide. That's a conversation worth having with your loan officer before you commit to a loan type.

Common VA funding fee myths

Myth: the lender is pocketing the funding fee. The fee goes directly to the VA. Your lender collects it and forwards it to the federal government. There is no scenario where the lender profits from it.

Myth: you can negotiate the fee away by choosing a different lender. The funding fee is set by federal law. It is not a lender fee. Shopping lenders will not change the rate or eliminate the fee. Only a legal exemption removes it.

Myth: if you paid the funding fee on your first VA loan, you're exempt on the second. Prior payment of the fee does not create an exemption. Subsequent use carries a higher rate, not a waiver.

Myth: the funding fee only applies when buying a home. VA cash out refinances and most IRRRLs carry their own funding fee. The rates differ from purchase loans, but the fee exists across all three transaction types.

Myth: a disability rating below 100% doesn't qualify for a waiver. Any service connected disability compensation qualifies, regardless of the percentage rating. This is probably the costliest misconception I see. Veterans with 10%, 30%, or 50% ratings are just as exempt as veterans rated at 100%.

If you want to understand how your VA entitlement and benefit eligibility work together, reading our How To Get a Certificate of Eligibility(COE) for a VA Loan and How VA Entitlement Works: A Complete Guide for Veterans articles are a good place to start.

Frequently asked questions

Is the VA funding fee tax-deductible?

The VA funding fee has historically been treated as mortgage points for tax purposes, which allowed it to be deducted in certain circumstances. However, tax treatment depends on current IRS rules, the specific way you paid the fee (upfront vs. financed), and your personal tax situation. I'm not a tax advisor, and I'd encourage you to ask a CPA or tax professional before assuming a deduction applies. Tax law in this area has changed more than once, and your eligibility to deduct it depends on factors beyond the loan itself.

What happens if I paid the VA funding fee but later found out I was exempt because my disability claim was approved retroactively?

You may be entitled to a refund. If your disability rating was backdated to a date that predates your closing, the VA can refund the funding fee you paid. This is not automatic. You need to contact the VA directly once your rating decision is issued and confirmed, and request the refund through the appropriate channel. Your lender can help you understand what documentation is needed, but the refund process runs through the VA, not the lender. This is another reason to stay on top of your claim status before closing when possible.

Can I avoid the VA funding fee by putting money down?

Yes.

A down payment of at least 5% reduces the funding fee.

A down payment of 10% or more reduces it further.

Do Reservists and National Guard members pay the same funding fee as active duty veterans?

As of recent Congressional adjustments, Reserve and National Guard members who meet VA loan eligibility requirements are subject to the same funding fee rates as regular active duty veterans for most loan types. That was not always the case; for years, Reserve and Guard borrowers paid a slightly higher rate. Confirm your specific military category with your loan officer when you apply, since the rules have changed over time and it's worth verifying which rates apply to your situation.

Does the VA funding fee apply to a VA IRRRL (streamline refinance)?

Yes. A VA IRRRL carries a funding fee of 0.50% of the loan amount. That rate is substantially lower than the rates for purchase loans and cash-out refinances, but it is not zero for most borrowers. Veterans who qualify for a disability-based waiver are exempt from the IRRRL funding fee just as they are from the purchase loan fee. The IRRRL is designed to be a lower-cost refinance option, and the reduced funding fee is part of what makes it efficient for veterans who qualify.

If I use my VA loan benefit a second time, does the funding fee rate ever reset to the first-use rate?

No. Once you have used your VA loan benefit, subsequent uses are subject to the higher subsequent use rate regardless of how much time has passed. The rate does not reset after a certain number of years or after paying off the prior loan. However, if you fully restore your VA entitlement after paying off a previous VA loan, the subsequent use rate still applies; restoration of entitlement is not the same as resetting your funding fee tier. The only way to avoid the subsequent use premium is to make a down payment of at least 5%, which brings the rate down to 1.50%, or 10%, which brings it to 1.25%.

If you're a veteran trying to understand what you'll actually owe at closing, complete our short Explore My Options questionnaire. We'll review your eligibility, funding fee status, potential exemptions, and estimated monthly payment so you can move forward with confidence. The numbers I've used here are illustrative, but your actual funding fee, loan balance, and monthly payment depend on your purchase price, down payment, use status, and current rates.